IRS delays implementing Form 1099-K $600 3rd party payment reporting threshold until 2023, relief for Gig Economy Self Employed and freelancer taxes

Small biz accountants, third-party settlement organizations, e-commerce platforms (including eBay, PayPal, Etsy, CashApp, and Venmo), and self-employed freelancers, sole proprietors and small businesses that use those platforms to sell their products and services got an early gift today. The Internal Revenue Service (IRS) announced a delay in the new 1099-K reporting threshold enacted by Congress as part of the American Rescue Plan of 2021 (ARPA).

Kelly Philips Erb, a Bloomberg Tax editor wrote “christmas came early this year for many taxpayers and tax professionals. Just before the holiday, the IRS announced that it would delay the revised controversial reporting requirement for third-party settlement organizations.

Reduced Form 1099-K Reporting Threshold AKA the Paypal Loophole

I wote about these proposed changes which were called the “Reduced Form 1099-K Reporting Threshold AKA the Paypal Loophole” the Covid-19 relief bill called the American Rescue Plan Act of 2021 (the “ARPA”) that Congress signed and passed into law in March includes a little-noticed provision that reduces the Form 1099-K reporting threshold for TPSOs to $600 regardless of the number of transactions. This provision will take effect next year, and is expected to raise $8.8 billion of tax revenue over the decade between 2022 and 2031.

As part of the act, the 1099-K reporting threshold was reduced from $20,000 to $600. This change was originally scheduled to take effect in 2022 and would have affected platforms, businesses, and individuals this coming tax season.

What this delay in 1099-K reporting means

As a result of this delay, the platforms and companies referenced above will not be required to report tax year 2022 transactions on a Form 1099-K to the IRS or the payee for the lower – $600 – threshold amount enacted by Congress as part of the ARPA.

The IRS guidance indicates that the calendar year 2022 will be a transition period for implementing the lowered threshold reporting for third-party settlement organizations (TPSOs), including Venmo, PayPal, and CashApp, that would have generated Form 1099-Ks for taxpayers.

The confusion revolves around reporting thresholds.

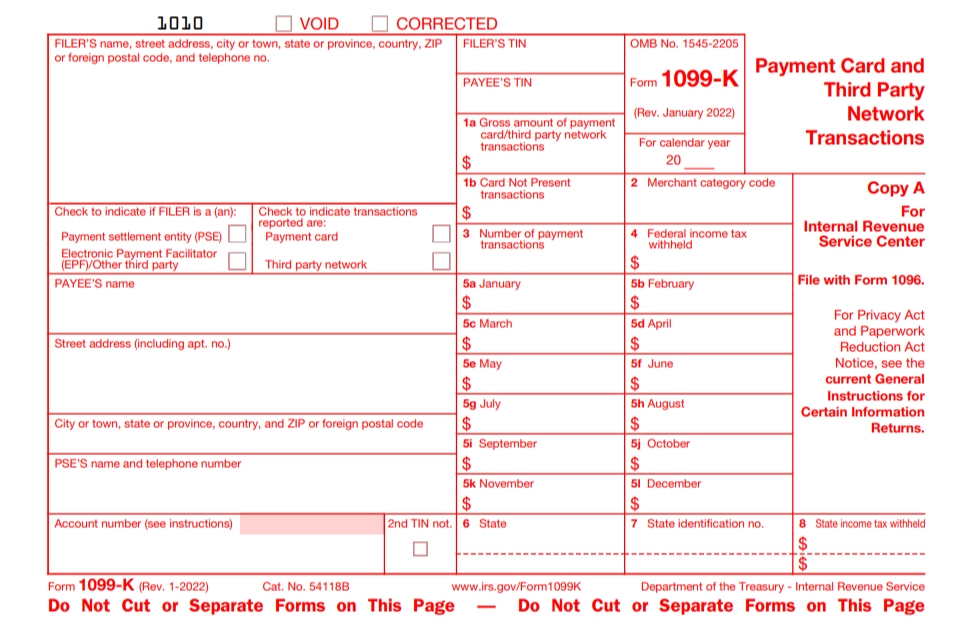

For years, taxpayers who provided certain goods or services worth more than $600 were responsible for issuing Form 1099-MISC. That changed in 2012 with the introduction of Form 1099-K.

Form 1099-K introduced a requirement for reportable payment transactions defined as payment card transactions or third-party network transactions. Payment card transactions include accepting a card—such as a gift card, credit card, or debit card—for goods or services. A third-party network transaction is one that is settled through a third-party payment network, such as PayPal or Venmo.

Form 1099-K requires reporting when payments total more than $20,000 and more than 200 transactions are settled through a third-party network. No threshold applies to payment card transactions.

As you can imagine, the gap between the “old” Form 1099-MISC reporting threshold and the Form 1099-K reporting threshold raised some eyebrows. The fix was a lower $600 threshold amount enacted as part of the American Rescue Plan of 2021. That new threshold was set to take effect in the 2022 tax year, meaning forms that would be distributed in early 2023.

Many feared the new threshold was too low

Taxpayers and tax professionals were concerned that the lower threshold would open the floodgates for Forms 1099-K, including those that reported personal transactions made on certain platforms. Personal transactions were never intended to be reported on individual tax returns—the law, as written, applies only to business transactions. The combination of a low threshold and misinformation about reporting requirements resulted in considerable confusion.

A number of fixes to the law were proposed. Days before a vote on the omnibus bill, Sen. Bill Hagerty (R-Tenn.) and Sen. Joe Manchin (D-W.Va.) announced an amendment that would have increased the threshold for Form 1099-K to $10,000. The amendment didn’t appear in the final version of the omnibus—but the clamor for an increased threshold grew.

The American Institute of Certified Public Accountants sent a letter to the Senate Finance Committee and the House Ways and Means Committee, expressing “deep concerns” about the threshold. The AICPA noted that the $600 threshold was based on Section 6041 of the tax code, established in 1954, and never adjusted for inflation.

A quick check on the numbers shows quite a boost. My math using the US Bureau of Labor Statistics inflation calculator shows that if the cost of living adjustments had been made, the threshold would be over $6,640.

The AICPA gave a nod to the National Taxpayers Union Foundation, which had recommended raising the threshold “to a level sufficient to exempt casual or low-level online activity.” A $5,000 threshold, they noted, would “make significant progress toward that goal while shielding taxpayers, platforms, and the IRS from some of the worst administrative fallout.”

Notice 2023-10 delays the new reporting requirements

Notice 2023-10 delays the reporting of transactions in excess of $600 to transactions that occur after calendar year 2022. The IRS refers to this as a “transition period” that is intended to facilitate an orderly transition for TPSO tax compliance and individual payee compliance with income tax reporting.

In the case of a third-party network transaction, a participating payee is any person who accepts payment from a third-party settlement organization for a business transaction.”

The rationale for the Congressional action in 2021 was felt to be necessary to enhance compliance. The IRS noted that tax compliance is higher when amounts are subject to information reporting, like the form 1099-K.

The agency does acknowledge that “it must be managed carefully to help ensure that 1099-Ks are only issued to taxpayers who should receive them. In addition, it’s important that taxpayers understand what to do as a result of this reporting, and tax preparers and software providers have the information they need to assist taxpayers.”

Tax professionals, these TPSOs, and others were very concerned about the complexity and confusion this reduction in 1099-K reporting will cause for both the companies and individual taxpayers.

Conclusion

A recent Forbes article contributor wrote “the change under the law is hugely important because tax compliance is higher when amounts are subject to information reporting, like the Form 1099-K. However, the IRS noted it must be managed carefully to help ensure that 1099-Ks are only issued to taxpayers who should receive them. In addition, it’s important that taxpayers understand what to do as a result of this reporting, and tax preparers and software providers have the information they need to assist taxpayers.”

Additional details on the delay will be available in the near future along with additional information to help taxpayers and the industry. For taxpayers who may have already received a 1099-K as a result of the statutory changes, the IRS is working rapidly to provide instructions and clarity so that taxpayers understand what to do. The IRS also noted that the existing 1099-K reporting threshold of $20,000 in payments from over 200 transactions will remain in effect.

Feel free to reach out to Thomas Huckabee CPA, for a free consultation to discuss the new tax compliance rules or with any other questions.

{kind=link}