Small business owners’ guide to the 2023 tax filing season

Here is a small business owner’s guide to the 2023 tax filing season. The volume and pace of tax changes over the past 5 years have been interesting. The 2017 overhaul has been followed by other law changes, including two major updates of retirement-account rules and a host of provisions responding to the Covid-19 pandemic. In addition, the Internal Revenue Service has issued guidance on key issues.

Every year inflation adjustments also shift the code. Given surging inflation in 2022, some of the changes for the tax year 2023 are especially large. For example, employees can elect to contribute $22,500 to 401(k)s and similar retirement plans for 2023, or $2,000 more than 2022. It’s both the largest dollar and percentage increase in this benefit to date, say tax specialists.

For filers preparing 2022 returns, the good news is that the tax code is entering a period of relative calm as confusing changes prompted by the pandemic have expired. However, many filers will also see smaller refunds because of these expirations.

For business owners (including 1099–K reporting)

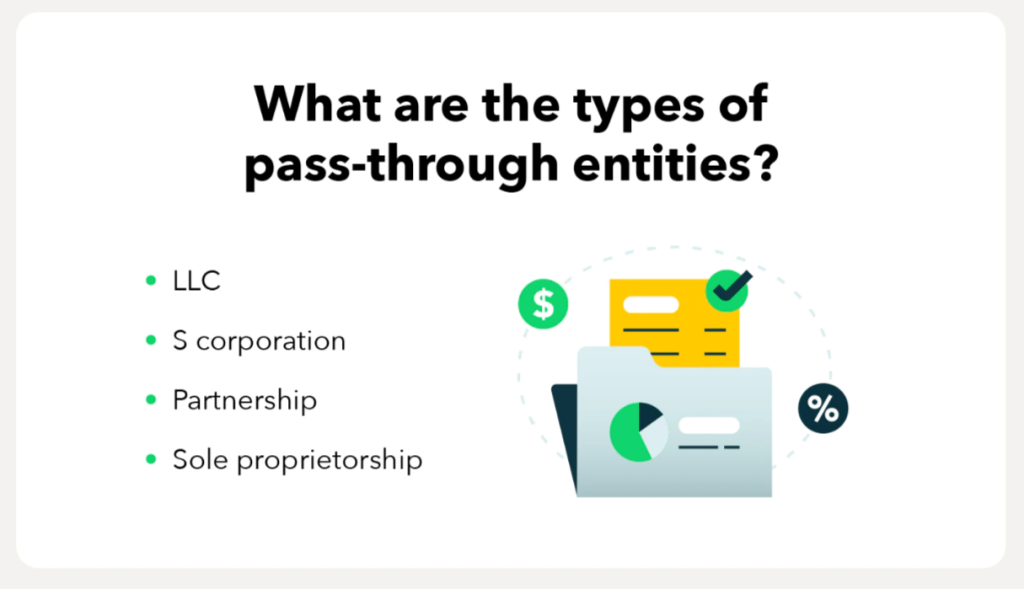

For most U.S. startups, private and small business owners, the political fighting over the corporate tax rate and taxation of foreign income does not matter to them. That is because most U.S. businesses are organized as so-called pass-through entities for tax purposes. This means the businesses’ income and expenses pass through to the owners’ individual tax returns. Any income taxes are paid at individual tax rates.

So everything that affects individual taxpayers also affects the owners of pass–through entities, which include S corporations, partnerships, limited liability companies and sole proprietorships.

The definition of a business owner can also be quite broad. Gig workers and others who are independent contractors are technically treated as business owners under the tax system. That comes with additional tax obligations because they must pay their own payroll taxes through the self-employment tax system.

Because businesses are taxed on their profits and not on their gross revenue, many business owners can deduct a variety of expenses that employees can’t deduct on their individual returns. That is so long as business owners keep careful records.

These business deductions can include costs related to driving, maintaining a home office, tax-preparation fees and business meals. In more than 20 states, many pass-through businesses can use special tax provisions to help avoid the federal $10,000 limit on deductions for state and local taxes.

Pass-through deduction

For many of these business owners, the most important tax-code feature is the special 20% deduction for pass-through businesses. Congress created this 20% deduction in 2017 as part of the tax cuts pushed by then-President Donald Trump. It was designed to give these owners an effective tax-rate cut just like the one corporations received. Like other pieces of that law, the deduction is scheduled to expire after 2025 and is under attack from Democrats. Given the divided state of government, no changes are likely before 2025.

In 2022, for individuals with taxable income up to $170,050 and married couples with taxable income up to $340,100, the pass-through deduction is unlimited, regardless of industry, employees and assets. Because of annual inflation adjustments, those numbers move up to $182,100 and $364,200 for tax year 2023.

Above those thresholds, there are limits. Specified service businesses—including medical practices and accounting firms—start losing the deduction. For others, the deduction is limited by a formula that takes into account wages paid and tangible assets. For more information, see IRS Publication 535.

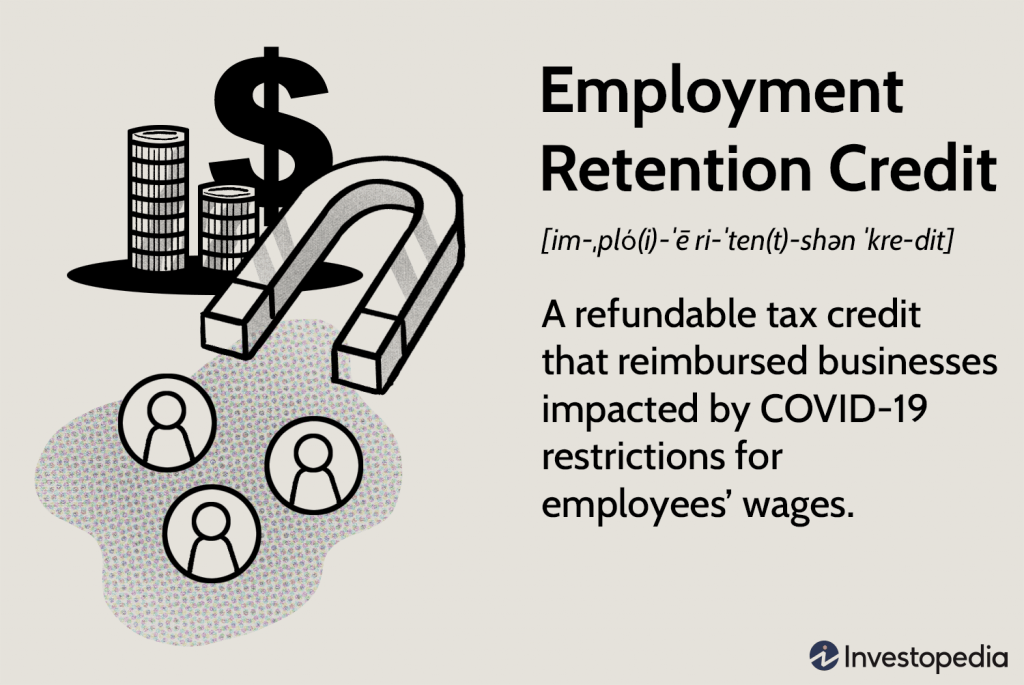

Employee retention credit

The coronavirus pandemic prompted Congress to make changes to business taxation to help companies cope with shrinking revenue as well as supply chain problems. But those have now largely expired. Other potential changes–particularly for multinational corporations–are potentially on the horizon.

Many smaller businesses can still be affected by Congress’s decisions to offer and then repeal the employee-retention tax credit that was created during the pandemic. Some are trying to claim it by amending prior years’ returns, and a cottage industry has sprung up to file those claims. The credit operated as a wage subsidy. For 2021, businesses could receive up to 70% of wages paid, up to $7,000 per employee per quarter.

Employers became eligible based on revenue declines or whether they were subject to government restrictions or closures. Smaller businesses can generally get the credit to cover their workers; larger businesses are limited in that they can generally get the credit only if they paid people not to work.

Congress repealed the credit effective after Sept. 30, 2021 for almost all businesses. This was done as part of the infrastructure legislation that became law in November of that year.

Eating out for work

Another pandemic-era provision expired at the end of 2022, and there was little effort in Congress to extend it. Under the provision, businesses were able to fully deduct the cost of restaurant meals, rather than face a 50% limit that had applied before. Mr. Trump had pushed for that idea to aid the struggling restaurant industry.

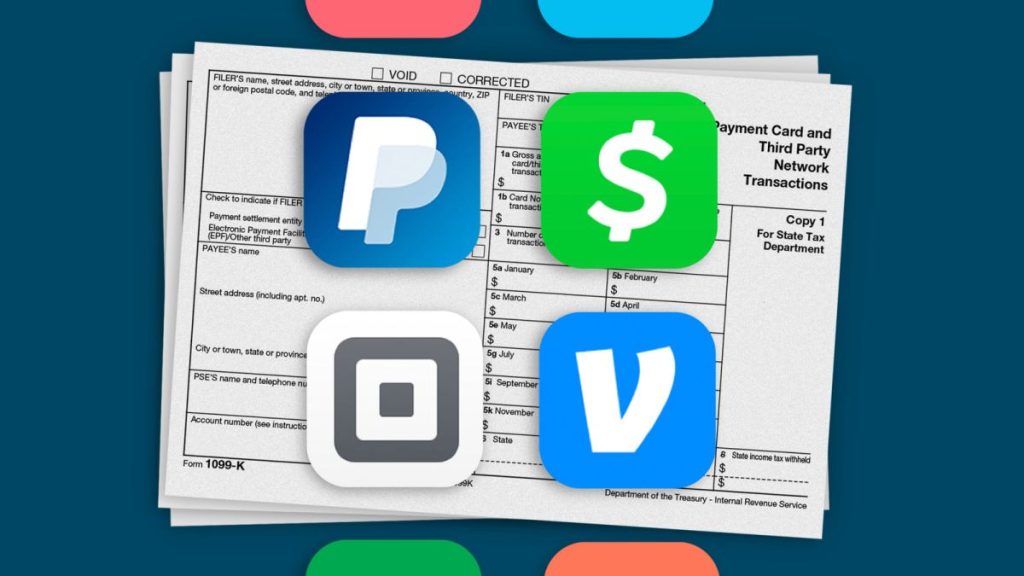

Digital payments

Another tax change going into effect in 2023 will affect businesses that receive payments through platforms such as PayPal and Venmo. Those services will begin sending information returns— on Form 1099-K—to users and to the IRS when transactions for goods and services exceed $600 in a year.

The plan, enacted by Congress in 2021, is aimed at people who conduct business using those payment systems, not at people who get reimbursements from friends and relatives. Those information returns will give the IRS more data about their business activities, and the agency intends to use the information. It doesn’t change the rules about whether such transactions amount to income, and that can vary depending on individual circumstances.

Before that change, 1099-K information returns were sent only when a particular user had more than $20,000 and 200 transactions. The $600 threshold was supposed to apply to transactions starting in 2022. In late December, the IRS delayed the implementation amid concerns from businesses and members of Congress.

The change is now scheduled to start for transactions in 2023, with 1099-K forms being sent to business owners in early 2024. Meanwhile, Congress may try to raise the threshold or further postpone the effective date. Current IRS guidance on 1099-K issues is here.

Interest costs and capital equipment

Changes from the 2017 tax law are still roiling businesses as the rules change. Starting in 2022, many businesses are required to amortize their research costs rather than deduct them immediately. Members of both parties favor repealing or delaying that change, but they haven’t been able to do so because of broader tax-policy disagreements.

Starting in 2022, large companies face even tighter limits on deducting their interest costs under a new formula. And a provision of the 2017 tax law that allowed 100% deductions for companies that purchase capital equipment has started to phase down in 2023. The benefit is now declining so that there is a first–year deduction worth 80% in 2023, 60% in 2024, 40% in 2025 and 20% in 2026. Smaller businesses have a similar–but permanent–provision for immediate write–offs.

Conclusion

Remember tax days are approaching but if you are not ready don’t panic you can always file for an extension this 2023 tax season. If you have any questions feel free to reach out to Huckabee CPA for a free consultation.

{kind=link}